Dan Gilbert Juggles Tenants, And Taxpayers Are On The Hook.

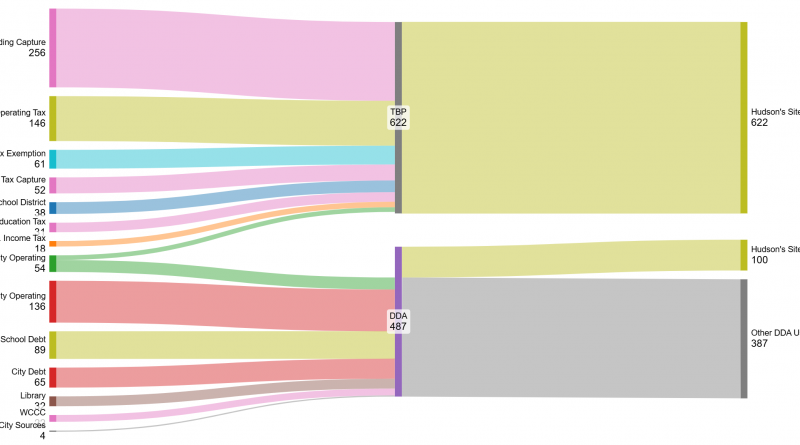

The University of Michigan says that the Hudson’s Site in Detroit will pay off the cost of the public subsidies, which amount to the better part of a billion dollars– by 2052. Is it worth it?

Read More