Not a day goes by in 2025 without some egregious display of incompetence, overtly contemptuous behavior, or general foolishness from the current government in Washington. I keep a list and I’ll eventually publish it, but I do have an item for every day at this point. Today, that item is the idea of federal underwriting for a 50-year mortgage, which Bill Pulte proposed over the weekend. There are a number of reasons why this is trash. We’ll unpack just a few: market pricing problems created by the 50-year, the relative meaninglessness of “equity” in a 50-year loan, as well as market challenges with the structure of interest rates for such a product.

Price Effects

If we recall approximately 273 years ago in the spring of 2025, White House Press Secretary Karoline Leavitt declared that tariffs were not a tax hike, but rather a tax break. Tariffs are, of course, a tax hike– because a tariff is a tax. But the Trump argument was that tariffs would incentivize domestic production and drive down prices. Economists point out that this isn’t exactly how it works. It takes time to reshore manufacturing, and the uncertainty and increased costs from the tariffs have actually undermined domestic manufacturing productivity more than they’ve helped it. There’s the other price-matching element here, which is that someone who sees their competitors’ prices now go up, will also likely raise their prices a bit, even if they’re still able to undercut them.

Changing the fundamental math of residential mortgages isn’t that different. A 50-year mortgage, by spreading out the cost over an additional 20-year term, means a lower monthly payment. But it’s entirely possible that someone, figuring a buyer can afford an additional $200 a month from that increased amortization, might well try and jack up the sale price, so the savings is less like $200 and more like $50. This is not a certainty, and it would only (likely) raise prices if the 50-year mortgage became a common tool. The increase in the prevalence of the 30-year mortgage seems to have accompanied much higher prices, but we know that this is probably as much of a feature as it is a bug.

Markets Struggle To Price Interest Rates Over A Half-Century

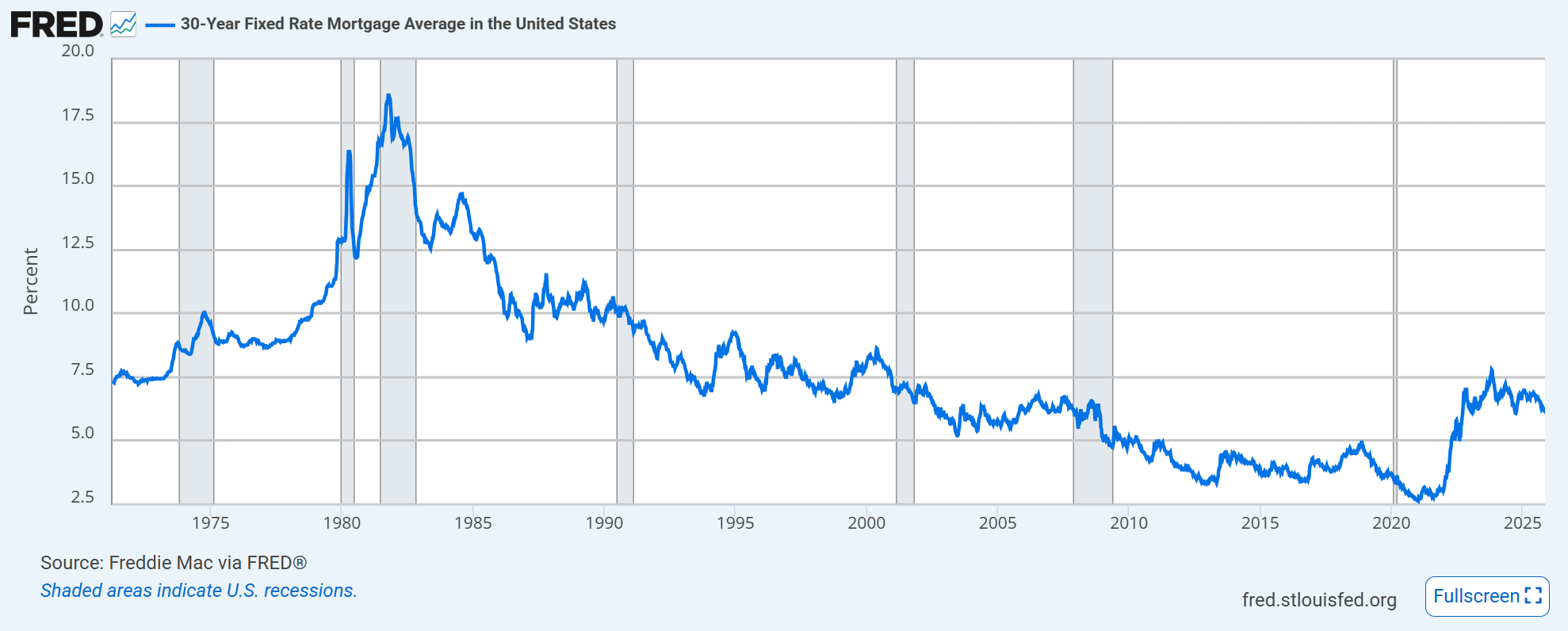

If we look at a chart from the St. Louis Federal Reserve below, we can see that interest rates aren’t stable over time. Woe be unto the homebuyer of the late 1970s into the 1990s, who could expect to pay as much as 10 or 15% or more on a mortgage. Of course, houses were much cheaper then, so there’s that tradeoff. But overall, the mortgage market is backed by a complex set of financial machinery that goes well beyond the federal entities of Freddie and Fannie. A lot of the liquidity that supplies mortgage loans is based on stability in markets, which is based on predictable enough rates of supply, demand, stable monetary supply, and limits on risk.

A 50-year mortgage imagines taking the chart below and drawing a straight line across it. If you averaged the rates over this entire time, you’d get a rate much higher than what consumers have been used to paying over the past 16 years.

It’s not clear how that would play out for the financial back-room processes of packaging mortgage loans and selling them on the markets. But suffice it to say that it’d be very hard to accurately price interest rates. When bankers and finance people face uncertainty, prices go up. Why? Risk costs money. So, if interest rates today are around 6.48%, there is virtually zero chance you’d get something that low. Would it translate to 7%? 8%? 9%? Who knows? It’s almost certainly going to exceed the average rate.

The Biggie: Zero Equity Loans

There are plenty of scenarios in which policymakers and bankers have teamed up to create “zero-equity” or very-little-money-down- loans in the name of affordability– typically a second mortgage layered with a conventional one to allow people to buy a house they might not otherwise be able to buy. Over a normal, 30-year mortgage, or even a 15-year, it can create equity, especially in ALICE populations.

But a 50-year mortgage would essentially turn homeownership into Housing-as-a-Service (also known as renting). If the argument in favor of homeownership is that you build equity, then you’re not building any equity here, beyond what you’ve had to put as a downpayment. This is a big critique in YIMBY discourse, which points out that hoarding wealth by preventing new construction or densification is a great wealth-building strategy— but one that crowds out any potential market entrants. In other words, we can think of homes as a great intergenerational wealth transfer machine, or we can think about lowering the monthly housing payment, but achieving the second one with a 50-year mortgage means there will be no intergenerational wealth transfer, because there will be no equity.

Mortgages frontload interest payments– that’s the way they are set up- so you wouldn’t get any appreciable equity into the deal until years and years into your loan. Banks might love it, because they’d make a lot more money. But going back to my second point? It’s possible that banks would jack up fees, knowing that their objective would be to offload these loans as quickly as possible to investors. If the only investor willing to buy these loans is a federal entity, guess who’s holding the bag in the event of, say, a market downturn? The taxpayer!

So, striking out a third time here.

Where Long Time Frames Do Make Sense

There is, at least theoretically, some sort of value for considering long-term financing. But it’s not for housing per se, at least not in the sense of “Joe Homebuyer Buy White Picket Home.” Rather, it’s possible to envision– and model (something I’m working on for some research)- financing for a very long-lived thing of some sort. Because a 50-year or 100-year financing horizon will outlive most of the people assembling it and, of course, earning any return on it, one would want to think about this exclusively for highly durable elements of the built environment.

We can think about a lot of elements of infrastructure or the built environment that we use consistently for a long time: think about railroads, tunnels, or even certain types of buildings. I’m thinking about the idea that projects that create more positive impact than they cost might be worth considering financing over such a long time frame. At least, that’s the hypothesis. We’ll see where I end up with it. My idea is that some of the most expensive parts of the built environment are the most durable, a category that could include commercial building foundations, climate-resilient infrastructure, etc.

So, perhaps there is some place for long-term financing somewhere.

But a 50-year mortgage? For the US housing market? Not a chance.